Once you have found your new car and have negotiated a price that works for both parties, you are no doubt excited to hit the road.

But first you have to pay for it!

Luckily, modern banking has made this part of the process incredibly easy for both the buyer and the seller no matter what the payment method.

In this article, we will discuss all payment methods available to you at the dealership. Some where you have to do nothing (settling a loan), to others where you have to be extremely careful (like carrying cash)!

Quick Summary

Some of the payment methods below are most suitable for smaller amounts of cash, like paying a holding deposit.

Most people are not comfortable walking around with $30,000 in their hand, and neither is the dealership!

So as a general summary, we can split each payment method into the following categories.

Paying the full purchase price:

- Loan proceeds

- Bank transfer

- Bank cheque

- Third-party platform escrow

Smaller holding deposits or funds to complete only:

- Cash

- Credit Card

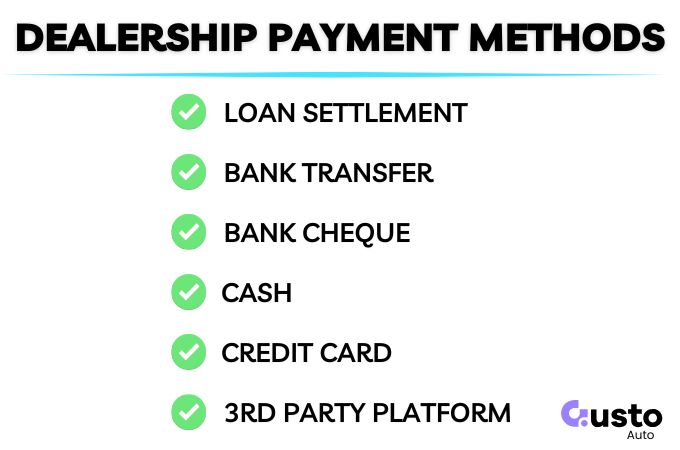

6 Payment Methods at a Car Dealership

While there are multiple ways to settle your payment for a new car, the reality is that the first two on this list make up the vast majority of dealership transactions.

They are the most convenient, cheapest, and the safest for all parties involved.

However, it can be good to know all your options in case you need to do a combination of payment methods to settle the full payment.

The most common scenario for multiple payment methods is if you are putting down a deposit to secure a vehicle while a car loan is being settled.

1. Loan Settlement Proceeds

If you are using a loan facility to buy your next car, then you will not need to be involved in the transfer of funds at all.

Once contracts are signed and the lender is ready to settle the loan, they will pay the dealership invoice directly in most cases.

As soon as the funds arrive in the dealership’s bank account, the vehicle will be ready for collection.

The main advantage of this payment method is that you are not handling any funds and will not be responsible for any errors that could happen along the way.

Such as an incorrect account number being used.

All other methods on this list are directed by the buyer and that will carry the responsibility to ensure the payment is completed successfully.

2. Bank Transfer

An electronic funds transfer is convenient, straightforward, secure, and widely accepted. The best part is it is fee free!

You will receive an invoice from the dealership that will include the purchase of the vehicle and any additional costs involved.

This will include the banking account details for the transfer.

All you need to do is transfer the amount nominated and the balance should arrive in the dealership’s account overnight. In some cases, the same day.

Given that a vehicle is a high-value purchase, you may need to adjust your daily transfer limit if you intend to pay the full amount in a single transaction.

Most banks default to a maximum of $5,000 to $10,000 a day. The cost of a vehicle can exceed this in most cases.

Your bank may have additional fraud controls that could be triggered when a large transfer is being completed to ensure the transaction is legitimate.

3. Bank Cheque

While bank cheques are a relic of decades gone by, some buyers still prefer to manage large purchases this way.

You will have to go to a bank branch and request a bank cheque in the nominated amount, and pay the required fee for the service from your bank.

The dealership will also have to bank the cheque after receiving it. So it could slow the whole transaction down if this step needs to be completed prior to releasing the vehicle.

While a bank cheque is as good as cash from the dealership’s point of view, in the digital age there is some fraud risk, and they are likely to insist on some kind of validation with the bank.

You can quickly see that the cost and inconvenience of this option is enough to turn most buyers off.

4. Cash

Believe it or not, some people still use cash! And in proportions large enough to purchase a vehicle.

However, it comes with obvious risks for both the buyer and the dealership.

Carrying large amounts of money is rarely a good idea. It could get lost, or stolen, and there is little recourse in the event of misfortune.

As a result, dealerships will often impose limits on how much cash they’re willing to accept.

It is a security risk and can introduce reporting complications when banking the funds.

While it is more common to pay a deposit of a few hundred dollars with cash, settling the full purchase price is rare and usually unnecessary.

5. Credit Card

Some dealerships allow part or full payment via credit card, offering buyers the advantage of convenience and potential rewards points.

This can be attractive if you have a card that provides cash-back or travel benefits.

However, dealerships often need to pass on merchant fees, which can add a significant surcharge to the transaction.

On purchases as large as a car, these fees can often outweigh the perks. But this is a very individual decision to make.

The limit of the card must also be able to accommodate the cost of the vehicle if you are settling the whole balance.

This is another payment method that is usually limited to an upfront deposit only.

6. Third Party Platform

Some online platforms, such as Carsales, offer a payment service that holds the funds in escrow until the handover of the vehicle.

This allows both parties to be protected from things like scams, or perhaps a vehicle that is not in the advertised condition at pickup.

However, this kind of service is more useful for private sales where there is more risk associated wth a transaction.

A licensed dealership is much more inclined to ensure a smooth transaction and a sound vehicle that is as advertised to protect its reputation.

Conclusion

The risk associated with transferring funds to a reputable and licensed car dealership is low. So, the payment method does not really matter and is flexible enough to suit your preferences.

Private sales can be less certain, and you would opt for a payment option with a paper trail in case something goes wrong.

At Gusto Auto, all we care about is that the transaction is completed in the most convenient way possible so that we can get you on the road as quickly as possible.